Lending processes are a complex mesh of customer management, risk assessment, collateral management, payments, and default management functions. Additional complexities also arise from the fact that multiple institutional parties are almost always involved, and that loans and their servicing can be sold or transferred.

Although solutions have been proposed using blockchain, complexities within the enterprise have largely been unaddressed, viz. streamlining intra-enterprise processes and data islands.

In this blog, we would like to propose a roadmap that helps with the immediate problems of constant reconciliation, transparency, and turn around time within an enterprise, while also paving the way to achieve the goals of collaboration across multiple organizations while preserving privacy and eliminating reconciliation. We will also present DeCredit, a solution that embodies these principles and provides a useful accelerator for enterprises looking to undertake this transformation. A special thanks to Manish Grover from Digital Asset for his valuable contributions and expertise.

The Framework

Presently, participants collaborate and manage data & processes in silos. They do this by often duplicating business rules and data stores. For example, within an organization, collections must be provided loan information to kick things off and then updated periodically. Similarly, in larger matrixed organizations, underwriting and risk departments maintain their own data islands which must be constantly synced. Digital interactions are often stored in their own islands.

Syncing these multiple islands requires data aggregation efforts and process orchestration which in turn often leads to costly operational delays, process breaks, and disrupted customer experiences.

When we consider interactions and data across multiple organizational parties, all of these challenges are magnified.

Note that “how” we exchange data between applications and organizations does not matter. For example, APIs and file transfers are common methods. Both of these on their own do not solve the problem of multiple data islands and the need for reconciliation.

For smaller organizations or those with a focused set of offerings, the issues with data duplication and processes can be mitigated to a certain degree by using packaged Lending Management Software. However, no business operates in a silo. Growth also necessitates constant change. So much of the investment that can be used for innovation is spent trying to manage basic data and process resiliency. In addition, there is decreased transparency and visibility into the end-to-end process for both institutional participants and the users themselves. For example, customers must create and manage multiple identities, lenders must manage KYC processes individually, credit agencies must ensure they receive the right data at the right time, and so on.

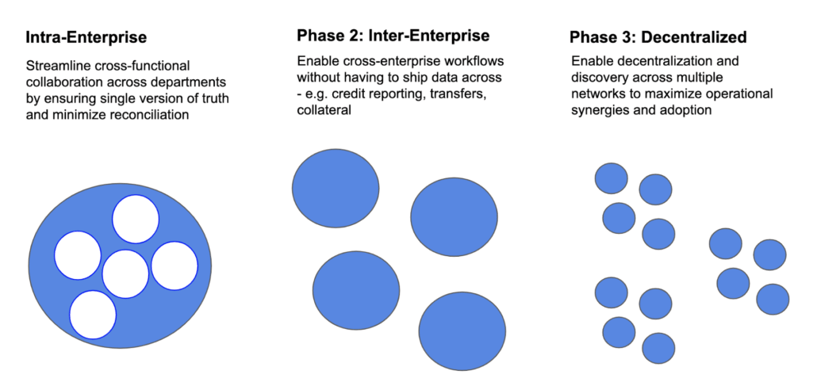

We think it’s useful to think of streamlining processes and driving innovation in the below 3 step model:

A smart contract-based approach using Daml (that can be run on both blockchains and databases) solves these immediate challenges and makes the lending process more efficient. The privacy aware, multi-party collaboration within and across enterprises that Daml enables reduces costs, paves the way for better analytics and AI, and provides the foundation for rapid business innovation. Daml has also a new learn section where you can begin to code online:

Our goal is to make the lending process easier and more secure through a platform where legal agreements can be established, physical touchpoints can be integrated, and relevant transactions can be updated to a shared ledger in real-time while maintaining confidentiality as needed.

This will be true for stakeholders within a single business entity, and also for multiple stakeholders from different organizations who need to collaborate on the underlying customer account or lending asset. For example, third-party organizations such as those that maintain and provide credit scores, manage collateral, provide legal services, and those that bridge the physical-virtual divide.

While such a smart contracts platform itself can be operated in a direct model where no intermediaries are needed, we note that many implementations may indeed designate a centralized and trusted operator of the network for management and administration - such as a governing organization within an enterprise. In addition, parties who provide services will need to be onboarded in the right way to promote confidence, regulatory compliance, and support to customers.

A few principles we started out with can be summarized as below. They apply to both decentralized lending as well as streamlining lending processes within an enterprise.

- Participating institutional parties and business divisions will have their individual data confidential

- Parties will not have to execute duplicate business processes and reconcile data

- Regulatory reporting and compliance will be baked in

- Operational rules and data semantics can be changed only after mutual agreement by parties thus addressing reconciliation challenges

- Parties will be able to separate their competitive advantage (pricing, products, analytics, customer experience, etc.) from the underlying plumbing

- Consumers will be in control of their identity and data (optional but this trend is growing stronger and being made possible everyday)

These principles allow us to solve for the immediate pain areas in the industry first, while also paving the way for a fully decentralized model.

Key Benefits of a Smart Contracts based Approach

By using Daml, the open-source smart contracts language from Digital Asset, we were able to achieve adherence to most of the above principles out of the box. For example, only the parties who have been defined as signatories and who have rights on the contracts have access to the confidential data. We did not need to layer on any additional plumbing. Multiple business process areas such as origination, repayments, collections etc, can be parties on the process, having access to only the data that is relevant to them, while an audit trail is automatically maintained.

Duplicate business processes arise in cases such as KYC where every institution must perform the validation for every new customer relationship. These costs can be collectively reduced (subject to the regulatory environment of course) using smart contracts. A KYC record can be made available upon request to a new entity without divulging the competitive nature of the previous customer relationship. (e.g. Lender A can request KYC but should not know about a customer relationship with Lender B). In fact, this is an area that can very well be positioned as the first milestone in the roadmap of decentralized lending that involves multiple organizations.

By onboarding parties such as credit agencies on to this network, significant overhead and errors with data reporting and privacy breaches can immediately be resolved. In addition, the costs of making this credit data available to consumers and other institutions upon request can also be much simplified. These agencies can simply be made observers on Daml smart contracts designed specifically to divulge specific data required for that purpose. Given that the same agency may support many organizations, synergies in data integration and technology plumbing can be realized quickly by using a smart contracts platform such as Daml. No additional actions need to be taken for reporting a new loan, or repayment status.

The connection from the virtual to the physical world is an important and practical part of a solution for the foreseeable future. A purist approach that only deals with digital transactions will not take us far. We can do this by onboarding trusted parties that hold the system of record or even intermediaries who act on their behalf to provide such services. Designing the smart contracts platform in this manner provides scalability of adoption, operational savings through automation as well as much needed accountability and transparency. For example, an inspection of collateral may need to be done offline, or a physical document may need to be brought into the system.

Finally, we acknowledge that not all systems can be integrated with such a credit platform. This could be because a system also performs other functionality, technological challenges, geographical constraints, or simply because of complex business change management considerations. We can observe this by looking at most enterprise technology landscapes today which are far from monolithic but have evolved through application integration. Fortunately, Daml allows for interoperability between systems. Such a decentralized credit application can execute transactions atomically with Daml models deployed by any of these non-participating entities. So while the primary platform may run on a smart contracts platform these external parties can continue to rely on traditional databases so long as they build interfaces using Daml smart contracts that speak to their legacy worlds.

DeCredit - Decentralized lending platform

Let us now talk about a platform that Knoldus built on Daml that outlines the above principles. In addition, we took the approach of making this solution ready to try and adopt. Our aim behind creating this application was to provide users with a way to carry out day-to-day transactions not only easily but also to give them a sense of security by recording the transactions on a decentralized ledger.

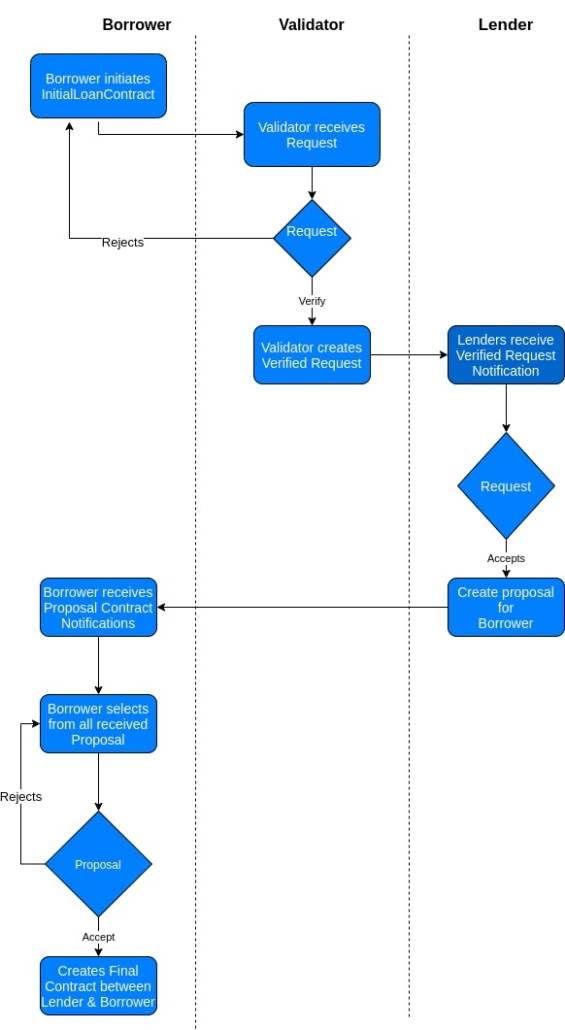

DeCredit is a Daml-powered decentralized loan lending application backed by digital collaterals in a peer-to-peer network. The borrower in need of funds can create a profile on the platform and initiate a loan request by setting one of their digital cryptocurrencies as collateral. DeCredit also supports other types of collateral that reside offline. The lenders can check existing loan requests and, based on the risk assessment, propose the amount and a desired rate of interest. The borrower can then choose from among the various proposals received and select the one that suits their needs, at which point the disbursement process starts.

DeCredit allows for the use of cryptocurrency as collateral because that’s easiest to validate and secure digitally without requiring intermediaries. However, this collateral model can be extended as outlined in the previous section. The use of Daml allows for end to end flow transparency, and easier regulatory reporting and compliance.

We also made use of the Daml Hub to deploy DeCredit. Using Daml Hub allowed us to deploy a public-facing app quickly without having to worry about authentication, performance, and security. Daml Hub completely abstracts away the underlying persistence layer so we can focus on the Daml ledger model and the rights & obligations of various parties.

For example, a loan application that must be approved by a lender looks like this using Daml. As you can see, using Daml simplifies the development dramatically while also allowing the business users to participate actively in the development process.

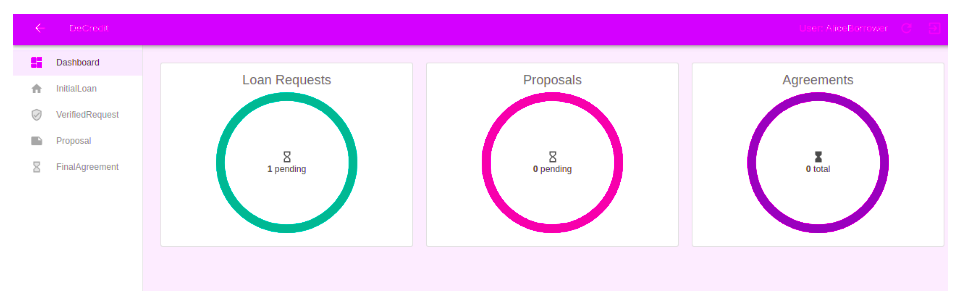

We were also able to add dashboards such as the below by pulling data from smart contracts. For more complex requirements, the data can be retrieved into an offline system (subject to Daml privacy and disclosure rules) where visualization and advanced analytics can be performed.

Conclusion

Lending processes that integrate smart contracts technology can realize tremendous operational and business benefits such as straight-through processing, easier regulatory reporting, simplified credit data management, removal of duplicate processes, and excellent user experience.

But we must consider the practical challenges of business change management and offer an achievable, incremental roadmap to adoption. We hope we have been able to demonstrate that in this blog. Starting with addressing intra-enterprise data islands, we moved to a trusted network where multiple organizations can participate and eliminate reconciliation, and finally we showed how to make this process completely decentralized with the right governance and regulatory framework built in. Using Daml allows us to achieve this roadmap rapidly while providing flexibility of deployment layer - blockchain for inter-enterprise, and DB for intra-enterprise. In addition, current applications can be integrated, not replaced, further reducing the complexity of the IT roadmap.

If you would like to discuss how to drive efficiencies in your lending process and technology portfolio using smart contracts or if you would like to know more about the DeCredit, please get in touch with us at Knoldus. Daml has also a new learning section where you can begin to code online: